Blue Bonds - Bringing Debt Markets to the Ocean Economy

This is the true mainstreaming of blue economy financing. It deserves to be celebrated.

When most people think of financial markets and products, they default to the stock market. After all, this is often the market most relevant to their personal financial situation - what’s happening to their 401(k) plan. Headlines about the daily fluctuations of the stock market dominate the financial news.

However, debt markets are larger than equity markets in the grand scheme of things. The availability of less sexy financial instruments like bonds, loans, and insurance significantly impacts the viability of projects, the survival of companies, and the transition of whole industries to a sustainable model.

Last year, headlines about very different debt structures brought the topic of blue bonds to mind. There were debt-for-nature swaps in Gabon and Ecuador and the first corporate blue bond issuance by an energy company, Orsted, the wind energy company. There was also the first publicly issued blue bond to hit the market in Japan (issued by Indonesia).

These are all very different use cases that fall under the umbrella of a blue bond. The broad definition of a blue bond is part of the challenge of growing the market, and clarity on that is also falling into place.

Instability in interest rates and debt markets led to a pullback in bond issuances last year. However, companies and countries are rushing back with interest rates falling and volatility settling down. Considering this recent trend, I thought it was a good time to look at what’s happening with blue bonds.

Understanding Debt Markets

The size of debt markets is staggering. That is why bringing these instruments into the blue economy toolkit is essential.

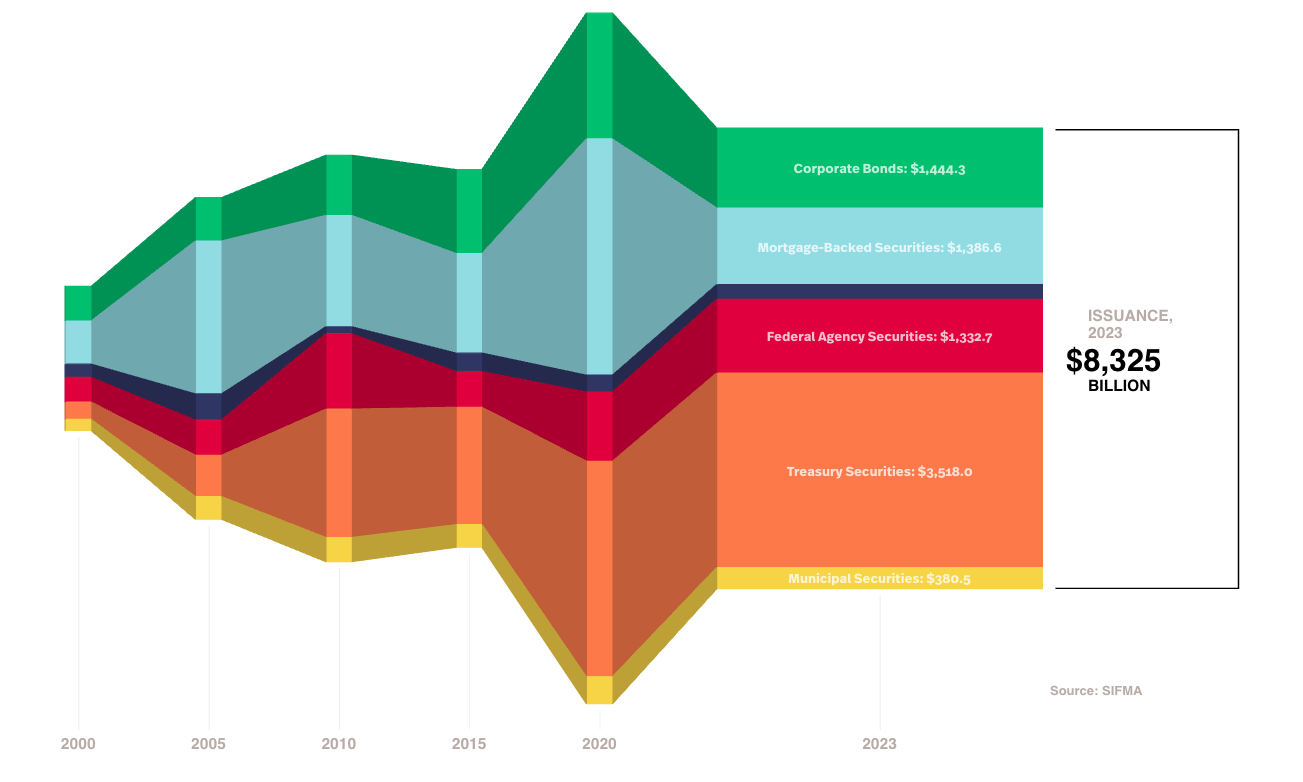

According to the Securities Industry and Financial Markets Association (SIFMA), total debt issuance in 2023 in the US was over $8 trillion, with roughly $1.5 trillion issued by corporations and $3.5 trillion in treasuries.

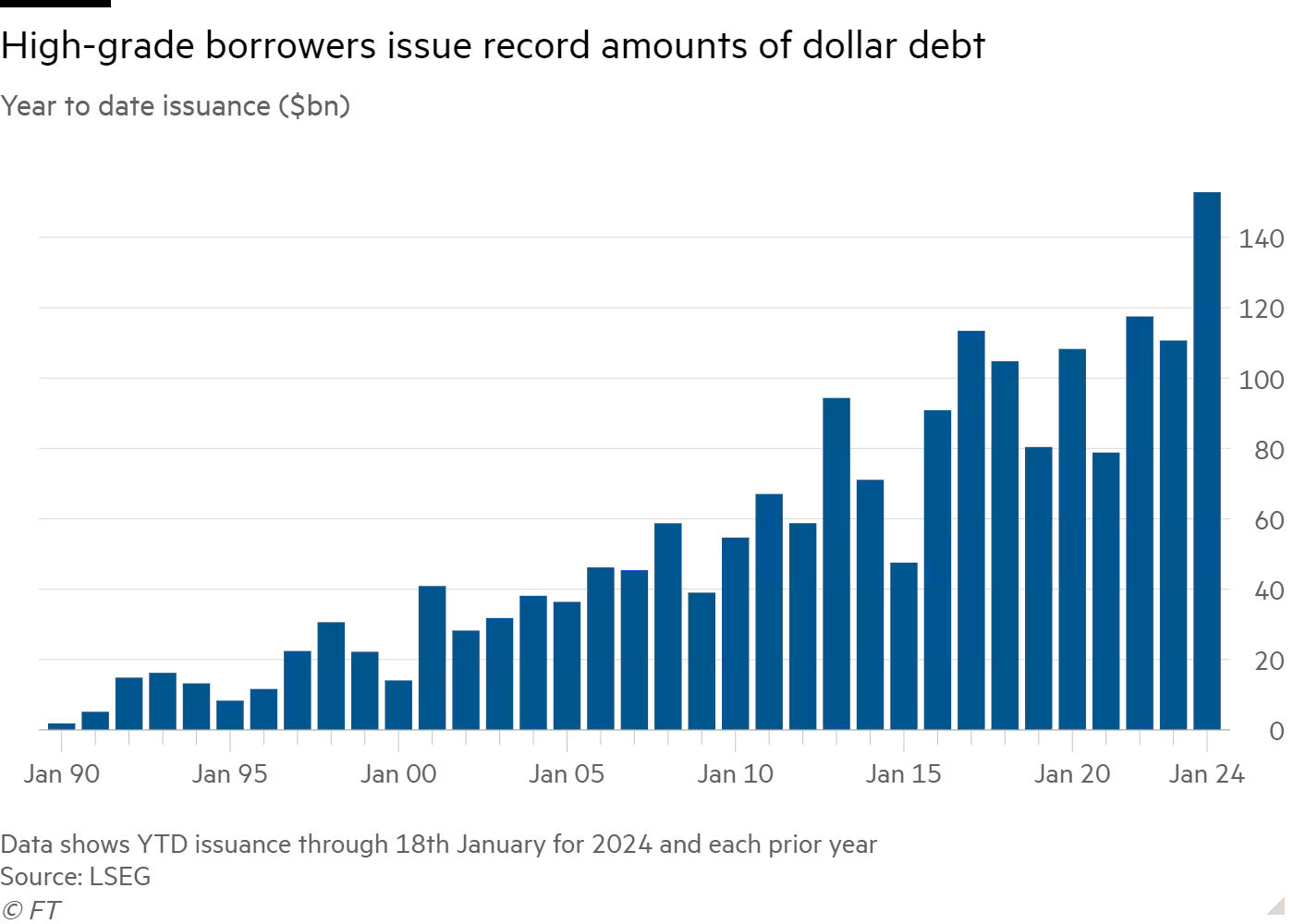

Recent headlines highlighted a surge in debt interest from investment-grade companies looking to take advantage of the pullback in interest rates from last year’s highs.

Interestingly, it isn’t just investment-grade companies looking to get in on the act. With the challenges and uncertainties of 2023 beginning to subside, even some frontier markets are eye-balling debt markets for 2024.

+Ivory Coast prepares to end Africa’s debt drought with dollar bond sale - FT

So, debt markets are opening up for everyone, from investment-grade corporations to frontier market economies in Africa. What does this mean for debt financing in the blue economy?

Green Bonds are Grabbing a Larger Slice

Blue bonds are a subset of green bonds. The difference is that the financing is used towards ocean-centric, “blue” projects instead of ones focused on general “sustainability.”

Therefore, it is useful to see how quickly the market’s appetite for green bonds grew in the decade since they were introduced.

Green bonds have grown to be a $1 trillion market yearly with a total sustainable debt now around $7 trillion.

Green bonds are still a relative novelty in the overall bond picture. Still, trends show investors’ appetite for them is there. New financial products are always met with caution, and investors will dip a toe before jumping in. But now that the concept is proven, the market is growing.

Funneling $7 trillion into sustainability is certainly nothing to laugh at.

The chart below shows how, after a slow start, green financing doubled between 2019 and 2020, then doubled again in 2021 to its peak of just over $1 trillion.

+Global Sustainable Bonds 2023 Issuance To Exceed $900 Billion - SPGlobal

There are a few macro reasons for the slowdown, namely the rise in interest rates that made the whole financial world pump the brakes in 2023.

But another key reason for the pause is that investors in early issuances now had the opportunity to look back and see if the funds were used for their intended purposes. Was there enough data gathered to measure the impact?

They were finally getting answers to whether impact bonds were impactful. The answers have been mixed, but data collection is improving.

While sustainable and green bond issuance slowed with the broader market, it is reasonable to think that the current resurgence in interest will also spill over to green debt. And if there is growth in green debt issuance, the nascent blue debt market should catch this macro tailwind.

History of Blue Bonds

“I know you are taking it in the teeth, but the first guy through the wall, he always gets bloody. Always.”

-John Henry, Moneyball

So, where is the blue bond market in its maturity/growth curve relative to green bonds?

The Republic of Seychelles issued the first blue bond in 2018. So, it’s worth remembering that this whole concept is only five years old. It’s a very new niche within a relatively new market.

Establishing new financial products is always difficult because you begin with a small, illiquid market. Without liquidity, it is impossible to move in and out of positions.

Early investors in these products take more risk and require much more due diligence than they need to with more established products.

The Seychelles bond was for USD 15 million, but it is critical to complete the first structure.

As was discussed in this podcast, Seychelles learned the lessons and made the innovations that helped the next ones that followed in its path:

In finance, no one wants to be the first one through the wall.

It is the risk department’s job to analyze all risks and unknowns. Each subsequent offering reduces those unknowns, and a liquid secondary market allows for adjustments along the way. And now that these first blue bonds are nearing redemption, their effectiveness can be measured against their stated goals.

Beyond liquidity, nailing down the definition, or taxonomy, of what makes a bond “blue” has also been an essential evolution since the Seychelles bond.

Despite the limited issuance of blue bonds, the variety within this subset of debt is significant. Participants include governments, corporations, and development banks. There are energy companies, seafood companies, and shipping companies. The bonds promise to benefit everything from water and wastewater to marine protected areas and aquaculture advancements.

That’s a lot for any potential investor to swallow.

What makes a bond blue?

The whole blue economy is still in the process of narrowing down definitions. In July, I wrote an article about the definitions of “blue economy” at various NGOs, development banks, and investment funds.

If people can’t agree on what the blue economy is, how can you agree on what a blue bond is? It’s tough to scale capital inflow when everything is bespoke. But these definitions are coming together. And when that happens, the speed at which things can move increases exponentially.

A perfect example of this acceleration is happening with the Central American Bank for Economic Integration (CABEI).

In December 2022, the CABEI published its blue bond taxonomy, clearly defining the types of projects eligible for the funds. This taxonomy was based on the “Blue Bond Reference Paper Investments” and “Sustainable Ocean Principles” published by the UN Global Compact and signed off on by a respected third party, Sustainalytics.

Within a week of publishing the taxonomy, CABEI successfully issued its first blue bond, and the second followed within a month.

The third and fourth blue bond issuances came within six months.

“I am thrilled to see the overwhelming market demand for CABEI’s blue bonds less than a month after publishing our Blue Taxonomy. It is evident that such instruments are emerging as a ground-breaking solution to mobilize capital and create sustainable business opportunities in ocean and freshwater conservancy.

Such high demand also comes to showcase the robustness and impact of our ESG projects that yield tangible benefits for both our borrowing member countries and our diversified investor base.”

+CABEI issues its second blue bond less than a month after publishing its Blue Taxonomy - BCIE.org

It took the Seychelles two years to get that first $15 million blue bond across the finish line. Thanks to their work, CABEI is off to the races.

Taxonomies Evolve

While CABEI took matters into their own hands and benefited from the upfront work, subsequent issuers will have the luxury of leaning on their work and a taxonomy recently published by the ICMA in conjunction with the IFC and Asian Development Bank.

+Blue Bonds: A practitioner’s guide - ICMA

+Sovereign Blue Bonds: A quick start guide - ADB

With these taxonomies, new interested issuers will be quicker to market. If these parties experience the same interest that the CABEI did in 2023, then the blue bond floodgates are about to open up.

Normalizing the Market

Normalizing the definitions of a blue bond has helped issuers move faster with larger bonds. This liquidity then attracts service providers to the segment that exists in other more mature market verticals.

These services are things we take for granted, but they aren’t there for new markets - in this case, indexes and funds.

Solactive, the German financial services firm, launched its blue bond index in 2023. And money management giant T. Rowe Price partnered with the IFC to launch the first blue bond-focused investment strategy.

Both institutional and retail investors rely on these types of services and structures to research and invest in various segments of the economy. As these services find their way into the blue economy, frictions to money coming in continue to iron out.

It becomes less exotic and custom. It begins to look like any other part of a thematic investment portfolio.

Current Market for Blue Bonds

Between 2018 and 2022, 26 blue bonds were issued with a total value of USD 5 billion. The average value was about $197 million per issuance. In 2023, I found nine blue bonds totaling $2.5 billion, half the previous combined total. The bonds ranged in size from about $500,000 to $1 billion. The average issuance size grew to about $280 million.

+The Blue Bond Market: A catalyst for ocean and water financing - Journal of Risk and Financial Management

I was able to pull data through 2022 from the report above. Still, I don’t have access to a Bloomberg terminal or Environmental Finance databases, so if anything, my 2023 number is understated. I’m bound to have missed something.

(If anyone wants to give me access to better data, I’m happy to talk!)

But still, you can see that blue bonds continued to grow despite a slight pullback in green bond issuances.

Blue Investing Goes Mainstream

I’ve written before questioning headlines claiming that blue economy investing has gone “mainstream” just because a couple of ETFs and some venture funds are focused on this investment thesis.

The emergence and acceptance of debt products, public issuances of bonds, and even bond funds to provide liquidity and access to bundles of blue bonds are vital to financing the transition to a sustainable blue economy.

This is the true mainstreaming of blue economy financing. It deserves to be celebrated.

Thanks for supporting this work.

If you enjoyed this post, be sure to like the post and share on your social feeds and with anyone you think would be interested in receiving Emerging Oceans!